A Summary of Your Rights Under

the Fair Credit Reporting Act

The Federal fair Credit Reporting Act (FCRA) is designed to promote accuracy, fairness, and privacy

of information in the files of every "consumer reporting agency" (CRA). Most CRAs are credit

bureaus that gather and sell information about you--such as if you pay your bills on time or have

filed bankruptcy--to creditors, employers, landlords, and other businesses. You can find the complete

text of the FCRA, 15 U.S.C. 1681-J 681 u, at the Federal Trade Commission's web site (http://

www.ftc.gov). The FCRA gives you specific rights, as outlined below. You may have additional rights

under state law. You may contact a state or local consumer protection agency or a state attorney

general to learn those rights.

• You must be told if information in your file has been used against you. Anyone who uses

information from a CRA to take action against you--such as denying an application for credit,

insurance, or employment--must tell you, and give you the name, address, and phone number of

the CRA that provided the consumer report.

• You can find out what is in your file. At your request, a CRA must give you the information in

your file, and a list of everyone who has requested it recently. There is no charge for the report if a

person has taken action against you because of information supplied by the CRA, if you request the

report within 60 days of receiving notice of the action. You also are entitled to one free report eve1y

12 months upon request if you certify that ( l) you are unemployed and plan to seek employment

within 60 days, (2) you are on welfare, or (3) your rep01t is inaccurate due to fraud. Otherwise, a

CRA may charge you up to $8.00.

• You can dispute inaccurate information with the CRA. If you tell a CRA that your file contains

inaccurate infom1ation, the CRA must investigate the items (usually within 30 days) by presenting to

its information source all relevant evidence you submit, unless your dispute is frivolous. The source

must review your evidence and report its findings to the CRA. (The source also must advise national

CRAs - to which it has provided the data - of any error.) The CRA must give you a written report of

the investigation, and a copy of your report if the investigation results in any change. If the CRAs

investigation does not resolve the dispute, you may add a brief statement to your file. The CRA must

normally include a summa1y of your statement in future reports. If an item is deleted or a dispute

statement is filed, you may ask that anyone who has recently received your report be notified of the

change.

• Inaccurate information must be corrected or deleted. A CRA must remove or connect

inaccurate or unverified information from its files, usually within 30 days after you dispute it.

However, the CRA is not required to remove accurate data from your file unless it is outdated (as

described below) or cannot be verified. If your dispute results in any change to your report, the CRA

cannot reinsert into your file a disputed item unless the information source verifies its accuracy and

completeness. In addition, the CRA must give you a written notice telling you it has reinstated the

item. The notice must include the name, address, and phone number of the information source.

• You can dispute inaccurate items with the source of the information. If you tell anyone--such

as a creditor who reports to a CRA--that you dispute an item, they may not then report the

information to a CRA without including a notice of your dispute. In addition, once you have notified

the source of the error in writing, it may not continue to rcp01t the information if it is, in fact, an

error.

• Outdated information may not be reported. In most c:iscs, a CRA may not report

negative information that is more than 7 years old; IO years for bankruptcies

• Access to your file is limited. A CRA may provide inform<1tion about you only to

people with a need recognized by the FCRA--usually to consider in application with a creditor.

insurer, employer, landlord, or other business.

• Your consent is required for reports that are provided to employers, or reports that

contain medical information. A CRA may not give out information about you to your

employer, or perspective employer, without your written consent. A CRA may not report

medical information about you to creditors, insurers, or employers without your pern1issio11.

You may choose to exclude your name from CRA lists fo1· unsolicited credit and insurance

offers. Creditors and insurers may use file information as the basis for sending you unsolicited

offers of credit or insurance. Such offers must include a toll-free phone number for you to

call if you want your name and add or removed from future lists. If you call, you must be

kept off the lists for 2 years. If you request, complete, and return the CRA fom1 provided

for this pu1vose, you must be taken off the lists indefinitely.

• You may seek damages from violators. If a CRA, a user or (in some cases) a provider of

CRA data, violates the FCRA, you may sue them in State or Federal court.

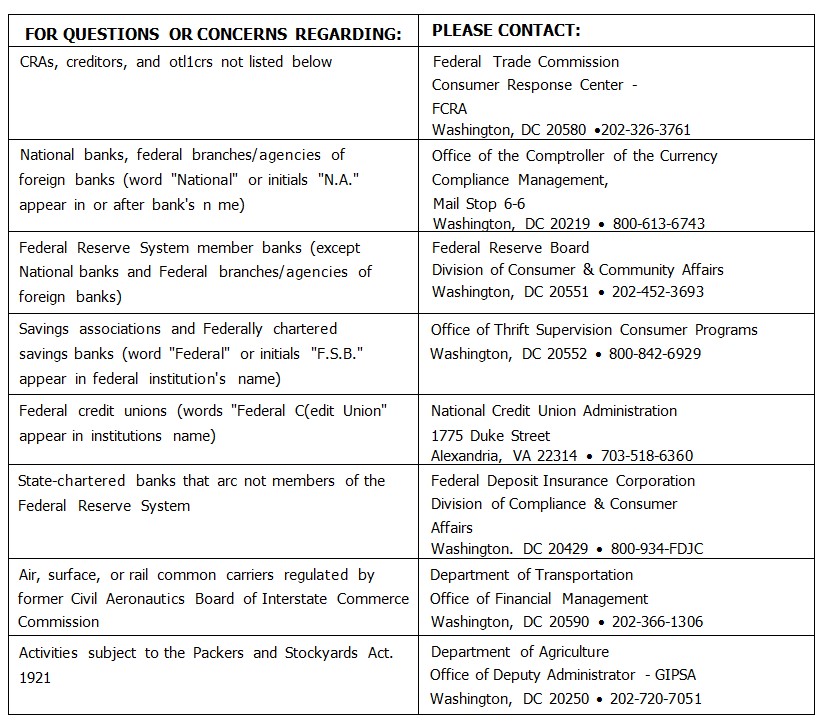

The FCRA gives several different Federal agencies authority to enforce the FCRA: